Let us suppose that you are an Irish civil service department, whose staff are employed on standard Irish civil service terms.

And let us suppose that your Secretary General’s 65th birthday was on 31 December 2013, by which time she had 40 years’ pensionable service. Her salary was €250,000 a year, so that’s the amount you (the department) paid to her in y/e 31 December 2013. Because of cutbacks, she is replaced, from 1 January 2014, by someone earning half that amount. So what is the cost of SecGens in 2014? Keep it simple: ignore employer’s PRSI and allowances and travel expenses and anything else.

Civil service pensions

In 2014, you will pay the new SecGen €125,000, half the old rate, but you will pay the retired SecGen €500,000, so your total expenditure on SecGens will rise from €250,000 to €625,000. [The timing may not be quite thus, but never mind.]

In 2015, the new SecGen will continue to get €125,000, but so will the old SecGen. So, even though your new SecGen gets half what the old one earned, the total cost to you remains the same.

And so on until the old SecGen dies. But if the new SecGen retires before that, you will have two retired SecGens drawing pensions and one even newer SecGen getting a salary ….

Under ordinary Irish civil service terms, someone who retires is entitled to a pension of one eightieth of final salary for every year of service, up to a maximum of forty years. So a SecGen who started, say, as a graduate entrant at the age of 25, stayed in the civil service and retired at age 65, would be entitled to a pension, for life, of half her final salary.

She would also be entitled to a lump sum of one and a half times her final salary. That’s why, on retiring, she gets an amount equal to twice her final salary: 1.5 times salary as a once-off lump sum plus 0.5 times as pension.

You could argue that that is an absurdly generous arrangement, but that’s not my point here: someone who started work 40 years ago under those conditions can’t be criticised for taking the money they’re entitled to, and it will be a long time before any revisions could take effect.

These pensions are defined benefit, non-contributory and unfunded: no money is put aside by either employees or the employer to meet pension payments in future years. It is assumed that the taxpayer will continue to meet the increasing costs.

Now, that’s all very well for the main-line civil service: it has been in existence for a long time; it’s very large, with a large pay bill; it has had SecGens retiring before and another retirement or two won’t greatly affect the overall cost.

But if you’re a relatively small organisation, dependent on the exchequer for most of your income but without any of getting extra money to pay for pensions, the retirement of one or two senior officials, or of larger numbers of lower-paid employees, could significantly increase your costs while doing nothing to improve your income or the amount of work you do.

That is happening to Waterways Ireland at the moment. I’ll give some details shortly, but first I want to get the pension scheme out of the way.

The woodchuck pension fund

Here is Wikipedia’s version of the tongue-twister about the woodchuck:

How much wood would a woodchuck chuck

if a woodchuck could chuck wood?

A woodchuck would chuck all the wood he could

if a woodchuck could chuck wood!

Coverage of the Waterways Ireland pension scheme in its annual reports reminds me of the woodchuck. I should say immediately that that is not a criticism of WI: it’s down to an accounting standard called FRS 17.

As far as I can make out, this standard requires WI to show in its accounts the entries that it would make for its pension fund, if it had a pension fund, even though it doesn’t have one. It does have a pension scheme, which I imagine sets out the rules about who is entitled to get what, but there is no pot of money put away, guarded by fierce trustees, to ensure that the pensioners of the future will get their money. Here is how I understand it; if I’m wrong (which wouldn’t be surprising), do please correct me in a Comment below.

WI’s balance sheet shows (for 2011) a liability of €66,432,000 and a balancing asset of the same amount; both of them are imaginary figures. Similarly, the income and expenditure account shows the amount that WI (in theory) should have paid in 2011 for the pension benefits that its staff accumulated in that year, along with an imaginary interest charge on its total liability. Those are then balanced by a figure called “Net deferred funding for pensions” which, at €4385000, is by far the largest component of WI’s “Other operating income”.

Obviously that lot would look better if it had corroborative detail to provide artistic verisimilitude, so the accountants or the pensions bods or someone did other calculations of currency translation charges and transfers in and out of the scheme and service costs and so on, all on a non-existent pension fund.

Now, as far as I can see, we can ignore all that. But there are two cash figures that are real and important:

- one is that WI staff paid (was it under the public service pension levy? or something else?) €230,000 in contributions in 2011, for which they will receive benefits of €2,744,000, ie twelve times what they put in

- the other is that in 2011 WI paid out €934,000 in actual pension

benefits to people who had retired by then. That presumably includes

any retirement lump sums.

Incidentally, WI’s 2011 accounts (the most recent available) make no mention of the North South Pension Scheme (see below), of which WI is a member. Perhaps the stuff in WI’s accounts is about its imaginary portion of a combined but equally imaginary fund under the North South Pension Scheme. The meetings of the NSPS CEO Pension Committee, which “exercises trustee-like functions” [seriously: see below], must be fun.

Not being an accountant (I feel I lack the necessary creativity), I am interested in the actual cost to WI of the benefits it pays out to folk who retire.

Retirements

I asked WI how many people retired in 2012 and 2013 and how many were expeected to retire in the next three years.

Figures for 2012 and 2013 are actual; those for later years are expected. Source: Waterways Ireland

Those who retired were:

- 2012: 3 lockkeepers, 1 boatperson, 1 director of marketing, 1 mechanical fitter, 1 general operative [GO] plant operator B, 1 preserved pensioner

- 2013: 1 chief executive, 1 clerical officer, 1 GO, 2 GO chargehands, 3 GO plant operator As, 1 GO plant operator B, 1 boatperson, 1 boatperson/skipper, 1 lockkeeper.

WI could not say what grades were expected to retire in 2014, 2015 and 2016. If they did, of course, I’d be able to guess which senior managers were about to retire; as it is, I have to rely on rumours. WI was able to predict the lump sum and pension payouts for 2014–2016, so I suspect it has a good idea who intends to retire.

The total number retiring in those five years is 81, which is about a quarter of the entire WI staff (currently 325). That’s a big proportion of the staff. No doubt it reflects the age profile of staff who transferred into the organisation but the figure may be boosted by the Hutton Push [see below].

Lump sums

Here is what WI expects to pay out in retirement lump sums in 2014, 2015 and 2016, and what it actually paid out in 2012 and 2013. Note the big increase in 2014. These sums are paid on retirement and are not recurring: in other words, they are made only to those who retire in the year in question.

Actual amounts for 2012–2013; predicted amounts for 2014–2016. Source: Waterways Ireland

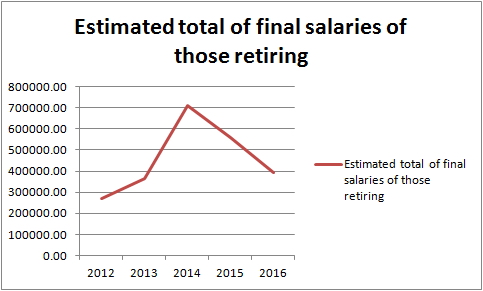

If all lump sums are 1.5 times final salary [something of which I can’t be certain], then we can work out the total of the final salaries of the retiring employees.

Source: actual and predicted lump sum payments divided by 1.5

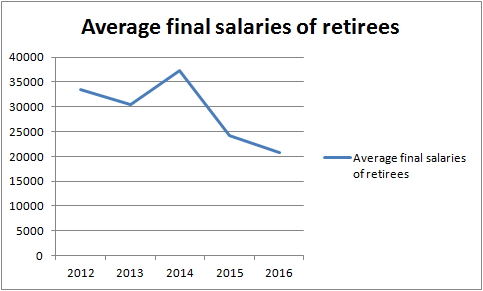

And, as we know the number of people expected to retire in each year, we can work out the average final salary for each year.

Source: actual and predicted total final salaries divided by numbers of retirees

It looks as if some senior staff may be expected to retire in 2014.

Annual pension payments

The lump sum amounts are paid only to those retiring in the year in question, whereas the annual pension payments include those to people who started drawing pensions in 2011 and earlier years. But the lump sums are once-off, whereas the annual payments will continue to increase as more people retire.

Source: Waterways Ireland figures for actual and predicted total pension pay-outs less lump sums

The effect on WI’s finances

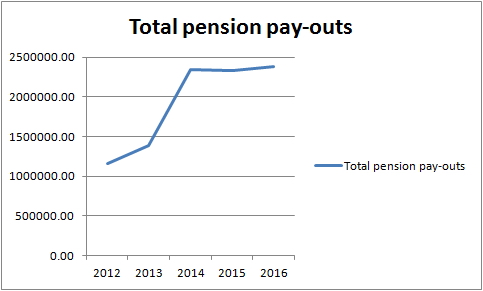

The totals of the lump sums and annual pension payments show how much WI has to pay out in each of the five years.

Totals of actual and predicted pension pay-outs. Source: Waterways Ireland

The figure shown in the 2011 accounts was €934000. By 2016, the total will be two and a half times that: €2377000.

Remember that this is an unfunded pension scheme, so the increase comes out of WI’s ordinary allocation of money from its sponsor departments. And that allocation will not be increased: both governments want to cut WI’s income, although one government wants to cut more than the other does. If the RoI government has its way, by 2016 WI’s income will be just under 66% of the 2010 figure: a cut of one third in six years.

According to the last available accounts, WI’s main cost is staff: €21,903,000 in 2011. But that figure includes €5769000 in pension costs, €934000 of which was benefits paid out while the rest was special magical imaginary payments to the pension fund; the real staff cost (excluding agency staff and employer PRSI/NIC contributions) was €14411000.

Between 2011 and 2016, the increase in pension costs means that an extra €1443000 has to be found and, as staff costs form the main element of WI’s expenditure, it is likely that the staff budget will bear much of the burden.

The Hutton push

One factor that may be prompting some WI staff to retire as soon as they can, thus pushing up the lump sum payments in 2014, is the possibility that some changes, recommended by the UK’s Independent Public Services Pensions Commission [the Hutton Commission], might be applied to the North South Pension Scheme that covers Waterways Ireland. On 30 April 2013 Martin McGuinness [SF, Mid-Ulster, Deputy First Minister] reported to the Northern Ireland Assembly on the North/South Ministerial Council [NSMC] institutional meeting held on the previous day.

Jim Allister [Traditional Unionist Voice, Antrim North] asked him about the pension scheme:

The pension scheme for those bodies entails lavish employer contributions. In one case, over 31% of salary is contributed by the employer and a mere 1·5% is contributed by the employee. When will that lavish squander be addressed by bringing the scheme into line with what exists in the Civil Service scheme? Is it good enough for it simply to be pushed back for another six months? Why not address it now instead of looking at it further down the road?

The ever-patient Martin McGuinness responded:

At the NSMC meeting on 28 March 2013, we noted that the NSMC approved an amendment to the North/South pension scheme, which means that increases to the scheme for benefits paid in the northern currency will be in line with the consumer price index. Prior to that, they were increased in line with the retail price index. The amendment ensures that the North/South pension scheme follows public sector pension policy, as agreed by the Executive.

We also noted that the two Finance Departments are in discussion about how to further amend the scheme. These amendments will ensure that northern members are not immune from pension reform. The first amendment will increase employee contributions on average from 1·5% by 3·2 percentage points. That will align with the employee rates payable from April 2014 in the principal Civil Service pension scheme here in the North. The second amendment will introduce, by April 2015, the wider Hutton reforms, such as the introduction of a career average revalued earnings scheme and a linkage between the North/South pension scheme age and the state pension age.

The scheme was raised in the Dáil on 17 December 2013 in a written question to the Department of Public Expenditure and Reform.

Dara Calleary [FF, Mayo] asked the minister:

[…] the discussions he has had in relation to the North/South pension scheme; if the proposed amendment rules as notified from officials in the Department of Finance and Personnel and his Department will apply to southern based employees of Waterways Ireland; and if he will make a statement on the matter.

The minister, Brendan Howlin [Labour, Wexford] replied:

Five of the six North/South Implementation Bodies, including Waterways Ireland, along with Tourism Ireland, operate the North/South Pension Scheme (NSPS). The Scheme is unique in covering public sector staff employed on both sides of the border; staff of the affiliated employers in this jurisdiction are automatically members of the Scheme. The Chief Executive Officers of the relevant NSPS bodies and Tourism Ireland meet as the NSPS CEO Pension Committee, which exercises trustee-like functions in relation to the Scheme.

As Minister for Public Expenditure and Reform, I am jointly responsible, along with the Northern Ireland Minister for Finance and Personnel, currently Mr Simon Hamilton, for the rules of the North/South Pension Scheme, and in particular for approving amendments which may be proposed to those rules. In exercise of my responsibilities in relation to the Scheme, I and my officials have engaged in correspondence and discussion about reforms to the NSPS rules with my counterpart Northern Ireland Minister and his officials.

Review and reform of existing pension arrangements, including public sector pension arrangements, has been an ongoing feature of the pensions landscape in Ireland and the UK over recent times. In this context it is natural that reforms to the North/South Pension Scheme would arise for consideration, and proposals in this regard have been discussed with the NSPS CEO Pension Committee.

Pending further development of these proposed reforms, and mindful that there is ongoing discussion with trade union interests on the proposed changes, I do not intend to elaborate at this juncture on the possible final specific content of the rule amendments which may arise. I can however confirm to the Deputy my intention that the changes will, to the extent that is consistent with legal norms in each jurisdiction, apply to southern and northern NSPS members alike, including staff of Waterways Ireland in this jurisdiction. This uniformity of application would reflect the fundamental all-Ireland character of the Scheme, to which successive Governments have been committed.

That doesn’t tell us much about the likely effects on the take-home pay of WI staff, or the pensions and lump sums of retired staff, and I have no inside information about what is proposed or likely. But you can see why WI staff who are near retirement age might be tempted to get out before their conditions are worsened.